Malaysia’s IRBM has granted stamp duty relief for employment contracts signed before 1 January 2025, with stamping required by 31 December 2025 for contracts signed during 2025. Self-assessment for stamp duty begins 1 January 2026. From that date, consolidated e-invoices are banned for transactions over RM10,000, though allowed until end-2025 unless transaction-specific e-invoices are required. The e-invoicing exemption threshold rises to RM500,000, with a 6-month deferral for businesses earning ≤ RM5 million. Phased e-invoicing starts in August 2024, with full rollout by 2027 based on revenue size.

Malaysia: Key Updates on Stamp Duty Relief & E-Invoicing

Public

Other countries

Author: Ljubica Blagojević

Category:

General information

Views:

5212

Content accuracy validation date:

03.07.2025

Content accuracy validation time:

08:17h

- Stamp Duty Relief for Employment Contracts

- Employment contracts signed before 1 January 2025 are exempt from stamp duty.

- The relief does not explicitly extend to other agreements like service or intragroup service agreements; businesses should carefully review these in light of increased IRBM scrutiny.

- For employment contracts signed during 2025, businesses have until 31 December 2025 to comply with stamping requirements.

- Companies should assess associated employment documents (e.g., increment letters) for stamp duty obligations under the Stamp Act 1949.

- Self-Assessment for Stamp Duty takes effect from 1 January 2026, so a broad compliance review is recommended beyond just employment contracts.

- Restriction on Consolidated e-Invoices

- Consolidated e-Invoices (which require less buyer data) are banned for transactions over RM10,000 starting 1 January 2026.

- Until 31 December 2025, consolidated e-Invoices remain permitted for transactions above RM10,000, except where transaction-specific e-Invoices are mandatory (e.g., motor vehicle sales, flight tickets, private charters, construction, and related materials).

- e-Invoicing Deferral and Exemptions

- The revenue threshold for exemption from e-Invoicing increases from RM150,000 to RM500,000, applicable to both incorporated and unincorporated businesses.

- If a payee is an individual not conducting business, payers must issue a Self-Billed e-Invoice (SBeI), regardless of income level.

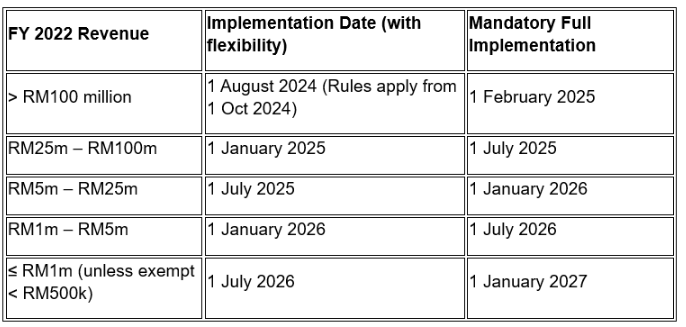

- The e-Invoicing timeline for businesses with annual revenue ≤ RM5 million is delayed by six months.

- Updated e-Invoicing Timeline

Notes:

- During the initial 6-month phase, consolidated e-Invoices are broadly permitted but non-compliance still triggers penalties.

- The RM500,000 exemption threshold is assessed annually. If crossed, e-Invoicing applies from Year 3.

- Group companies may be excluded from exemption.

- New businesses post-2022 follow a default start date of 1 July 2026, subject to exemptions.

Analysis:

- These updates signal IRBM’s stricter oversight on both stamp duty and digital tax reporting.

- Employers and businesses must conduct comprehensive reviews, especially regarding contracts, group structures, and transaction values.

- The phased e-Invoicing rollout provides flexibility, but businesses should not delay preparations given penalties still apply during transition periods.

- Particular attention is required for fragmented payments, individual recipients, and ensuring proper issuance of SBeI where needed.

Other news from Other countries

UAE: TRN vs. VAT Number: What’s the Real Difference?

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

In the UAE, the Tax Registration Number (TRN) and VAT number are a single 15-digit code issued by the FTA, necessary for VAT compliance. Registration is mandatory for taxable turnover exceeding AED 375,000, with voluntary registration allowed at AED 187,500. Operating without a TRN or using an incorrect one may incur penalties up to AED 5,000. The TRN is essential for charging and reclaiming 5% VA... Read more

UAE Businesses Urged to Prepare for Mandatory E-Invoicing as July 1 Deadline Approaches

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

UAE businesses must prepare for mandatory e-invoicing by July 1, 2026, selecting accredited service providers. The phased rollout starts January 1, 2027, enhancing VAT processing with structured, real-time invoice formats. UAE businesses are entering a critical preparation phase for mandatory e-invoicing, with July 1, 2026 set as the main deadline to select an accredited service provider (ASP). T... Read more

UAE Launches Optional B2B Peppol 4‑Corner E‑Invoicing

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

The UAE launched an optional B2B 4-corner Peppol e-invoicing framework, allowing suppliers and buyers to exchange structured invoices via Accredited Service Providers. This model precedes the mandatory 5-corner system in 2027, integrating the Federal Tax Authority. Businesses must comply with Peppol standards via the EmaraTax platform, ensuring early adoption for smoother transitions and complianc... Read more

Colombia’s Electronic Invoicing (E-Invoicing) Regime – Concise Briefing

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

Colombia has a comprehensive real-time e-invoicing system overseen by DIAN, requiring digitization of commercial transactions. All VAT-registered businesses must issue Factura Electrónica de Venta (FEV) for B2B and B2G transactions, with real-time clearance mandated since November 2020. Consumers also receive electronic receipts. Exports utilize a special electronic invoice, while imports require... Read more

UAE Launches Optional B2B Peppol 4‑Corner E‑Invoicing

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

The UAE launched an optional B2B 4-corner Peppol e-invoicing framework, allowing suppliers and buyers to exchange structured invoices via Accredited Service Providers. This model precedes the mandatory 5-corner system in 2027, integrating the Federal Tax Authority. Businesses must comply with Peppol standards via the EmaraTax platform, ensuring early adoption for smoother transitions and complianc... Read more

Chile Extends Deadline for Dispatch Guide and E‑Invoice Requirements

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

Chile's tax office postponed the implementation of new dispatch guidelines and invoice regulations to November 1, 2026, giving companies additional time for compliance preparation. The introduction of new regulations for dispatch guidelines and invoices used in the transfer of goods has been postponed by Chile's tax office. Exempt Resolution No. 52, announced by the Servicio de Impuestos Internos... Read more

ZATCA E‑Invoicing Rules in Saudi Arabia Explained

Public

Other countries

Author: Ema Stamenković

Other countries

Author: Ema Stamenković

Saudi Arabia’s ZATCA is mandating e-invoicing via its Fatoora platform to enhance transparency. Phase 1, completed in December 2021, introduced electronic invoicing. Phase 2, rolling out, includes B2B/B2G validations and B2C tax reporting. Saudi Arabia is progressively rolling out mandatory e-invoicing and e-reporting requirements for all businesses, led by the Zakat, Tax and Customs Authority (ZA... Read more